GEE GROUP ($JOB) | ~ 150% Upside

Do your own Due Diligence. The author is invested in GEE GROUP (NYSE: JOB).

First of all, I did not generate that idea on my own but found the initial investment thesis on www.valueinvestorsclub.com.

The thesis is very compelling as it fits exactly into my investment framework. You get this Cigar Butt $ for 0.54c with the optionality to become a good compounder.

GEE is cheap. It is cheap for a few reasons:

It’s small ($60m MC) and therefore obscure.

It performed historically poorly (-85% over the last 5 years).

It doesn’t screen well trading at ~5000+ times earnings.

BUT GEE resolved their biggest issue - the $56m debt with an interest rate of whooping 16%(!), and now trades at approximately 5x forward EV/FCF.

GEE is a roll-up that acquires staffing companies. As of today, the business has 10 business units and provides headhunting services (or direct hire placement services [15%]) and permanent and temporary staffing (85%).

The beauty of this business is that the permanent and temporary staffing are recurring. While customers can cancel their contracts anytime, they won’t do it as long as the economy is doing good and they demand professionals to do work in IT and Engineering, accounting, and finance.

That means, that revenues are easy to forecast (as long as we do not have a third world war or another big bank files a bankruptcy).

Here’s how the two business units - headhunting & permanent and temporary staffing, work.

Headhunting: The Headhunting division is a service they offer to corporates looking for employees. Corporates hire GEE Group to look and approach potential targets. After GEE finds a fit that is hired by their customer, they receive a success fee. Usually a % of the annual income, for example, 30%. This is a project business and should be more fluctuating.

Permanent & Temporary Staffing: This business is different. Over time, staffing companies build relationships with employees. They rent out those employees to companies for an amount x per h. For example, a GEE customer hires an IT Engineer for €100/h. GEE pays the Engineer a salary of $70/h. The difference of $30/h is GEE’s gross margin per hour.

The company had historical debt issues after it acquired SNI in 2017 for $86m via a reverse take-over.

Part of it was financed through the issuance of 5,926,000 Series B Convertible Preferred Stock to SNI shareholders worth $28.800m that could be converted anytime into stocks and another $12.5m convertible subordinated notes and another bank loan.

Nevertheless, I have to admit that I struggle to reconcile and understand the debt structure at that time. Therefore, I skip this part for now.

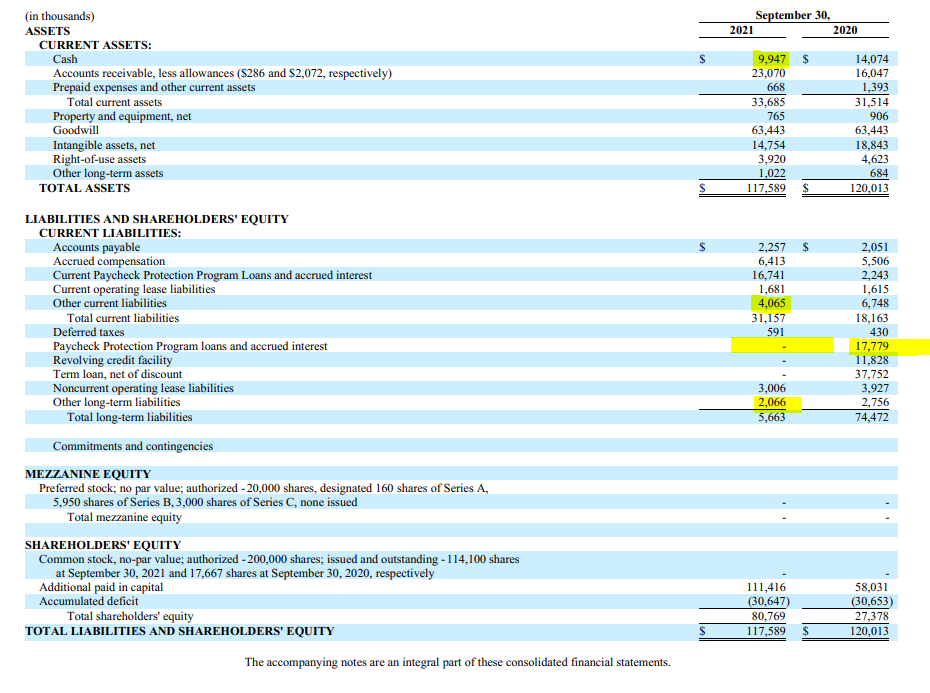

Without spending much more time on the financing and the debt structure, all we have to understand is that in 2021 GEE offered shares and paid back the loans. The share count increased from 9.879m shares to 114m shares as of today. The huge historical interest expenses vanished and for the first time, the business has a healthy balance sheet and earns a nice after tax profit.

The Math Behind GEE GROUP

In 2021, the business earned $148m in revenue and an operating profit of $6.5m. We assume that they manage to maintain revenue and profit going forward.

From historical acquisitions, they book amortizations of intangible assets. Those amortizations have a book value of $14.754m or are worth $3.1m in tax shields (21% Tax Rate on $14.754m).

GEE Group has another $37.5m in Net Operating Losses (NOLs). As far as I understand from the statement below, the $17.7m already expired, but we still have $19.8m worth of a tax shield of $4.15m.

On the balance sheet, we see that the Paycheck Protection Program Loan has been fully forgiven and the business has another $10m in cash.

Let’s assume that GEE manages to maintain current revenue and profitability. We have $6.5m in EBIT and we add the $4.089m in amortizations on top. EBITA is around $10.6m. We apply a tax rate of 21% and get to ~ $8.37m in NOPAT.

As of writing, there are 114,1m shares outstanding. So we have $8.37m or $0.0733 per share in NOPAT.

On top of that, we will have a further $0.0733/share in cash at the end of the year 2022. I assume, that most of the current cash on the balance sheet is required to run the business and finance working capital.

What’s left is the $3.1m tax shield from amortizations or $0.027/share and the $4.15m tax shield from the NOLs or $0.0363/share.

As of writing, the share price is at $0.54/share. $0.54 - $0.027 - $0.0363 - $0.0733 = $0.4034/share.

Divide the $0.4034 by $0.0733 in EPS and we get to a P/E multiple of 5.5x. Peers like Robert Half trade a 22x NTM P/E, Adecco at 8x, and Page Group at 14x. The average is 14x NTM P/E. Therefore, we have an upside of ~ 150%.

We already have a catalyst. As assumed, the former interest expenses vanished in the 1Q 2022 leaving a clean profit for the first time since 2017.

Disclosure: I do own shares in GEE GROUP at a purchase price between $0.52 and $0.60

Further information:

https://www.valueinvestorsclub.com/idea/GEE_GROUP_INC/2048142874

Thanks Paul for bringing this to my attention. So the PPP loan was forgiven and is being recognized as nearly 16.8 million in net income for 2022. So unless I am mistaken, this accounting will basically zero-out the NOL carryovers, right?

Still a compelling thesis. I'm not feeling confident yet about what the market re-rate might be though on a P/E level. I still need to complete my own research on this to get a better gauge on the potential upside.

Cheers!

Hi Paul, It looks like you are adding the entire amortization. What is the amortization actually expensing? and how do you know that it wont be a real cash expense going forward?