Do your own Due Diligence. The author (me) is invested in Northern Bear (AIM: NTBR). I own shares and if you think about buying shares of this business keep in mind that even a small investment from your side will move the share price due to the low liquidity of shares. It's not easy to liquidate if you want to get out.

Part I: Turning a Value Trap into a Value Investment: Northern Bear PLC (AIM: NTBR)

If you haven’t read Part I yet feel free to leave a visit:

If NTBR wants to realize a multiple expansion, the overall business quality, liquidity of shares, and capital allocation have to improve.

In the following, I want to introduce you to the subsidiaries of NTBR and show you a playbook that, I believe, would improve the business quality and return shareholder value.

NTBR Playbook:

Divest or cash out and shut down the non-core assets

Divest the bad assets,

Maintain the cash generative businesses,

Invest in the good assets

Acquire mom & pops and (Part III)

increase liquidity. (Part III)

A1 INDUSTRIAL TRUCKS

Let’s start with the non-core business. NTBR is the owner of A1 Industrial Trucks Limited (“A1”). A1 is a forklift and cleaning machine sales, rental, and services business, which does not fit into the construction portfolio (at least I do not know why it should be considered construction-related).

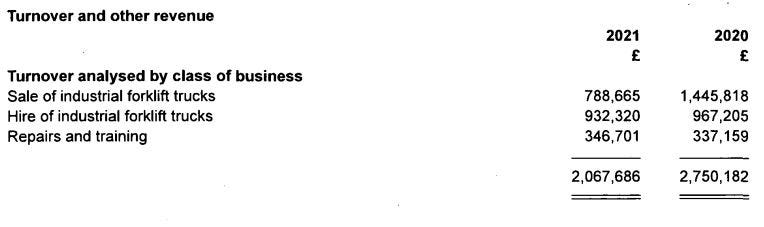

The gross profit of the business is declining and so are the earnings. A1 buys forklifts and leases them out. In the latest financials, A1 reports that repairs, training, and leases are around 60% of the total revenue.

According to A1’s website, A1 owns more than 500 forklifts and charges at least £60 per week. If we divide the £932.320 by (£60 x 52 weeks) we get to a maximum of 300 forklifts that are leased out to their customers. Either the business has only 300 or the utilization is low and would imply that the business is underperforming.

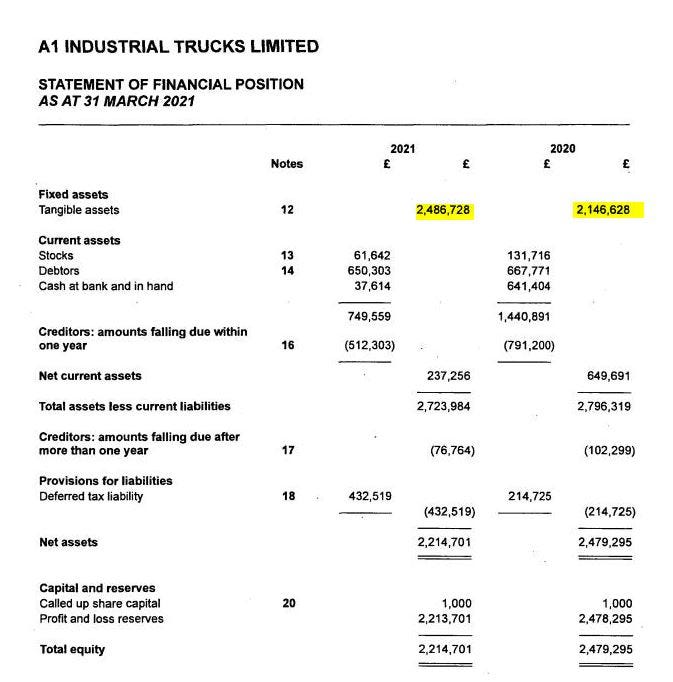

A1 has £2.5m tangible assets on the balance sheet and therefore is responsible for ca. 70% of NTBR’s £3.5m total tangible assets.

Therefore, A1 is an asset-heavy business with bad economics. The business is hardly making any money without the sale of forklifts. A1 has to pay the forklifts in advance and receives leasing payments afterwards. Very unfavorable terms to run a business.

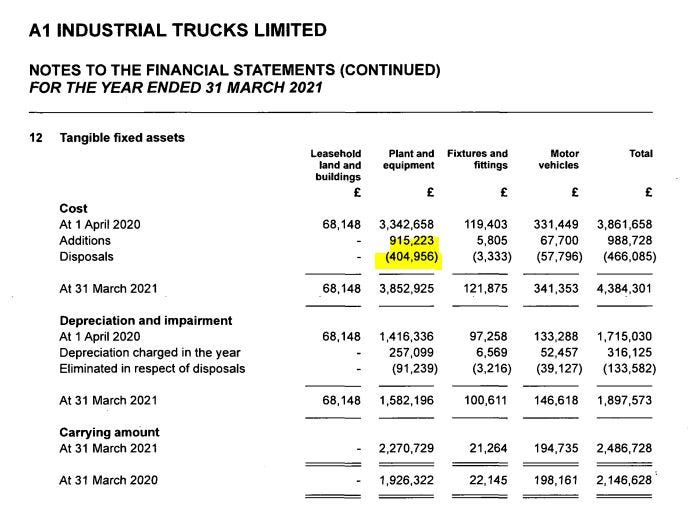

In 2020 and 2021, NTBR’s capital expenditures increased from £580k in 2019 to £1.15m in 2020 and £1.2m in 2021.

In 2020/2021, A1 added £915k in plant and equipment and in total £988k implying that 82% of NTBR’s group property, plant, and equipment capital expenditure is related to the A1 business unit.

My suggestion would be to either

sell the company or

scale the business down, stop investing in it, sell the whole inventory of forklifts, and close down the company.

After getting rid of A1, NTBR becomes an asset and CAPEX light business.

CONSTRUCTION BUSINESSES

The construction business unit should be divested. Northern Bear Building Services, MGM, and H. Peel & Sons contain unnecessary risks. All of the businesses are construction-related. Those refurbish and maintain buildings.

The issue here is that the margins are very narrow, the business is commoditized and the inherent risks are high. “Percentage of Completion” accounting is another risk. So far, I couldn’t observe any signs that would point towards a “completion of account” fraud, but it maintains a risk.

Another risk is a miscalculation of projects as we have seen with Kinovo. The low margins (which are lower than its peers) leave close to no room for project calculation errors and due to the size of the receivables, a mismanaged project could blow up one of the subsidiaries.

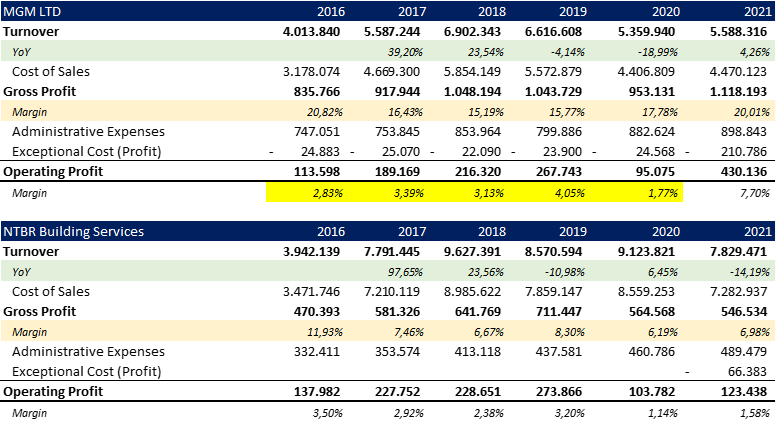

The acquisition of H. Peel & Sons was obviously too expensive. The company earned a profit before tax of 0.5m at the end of August 2016.

The year after, the operating profit went down to 270k. In 2018, the operating profit went up again and closed down lower in 2019.

I assume that there have been some real mistakes during the due diligence and that the management is not experienced in handling acquisitions. In retrospect, the whole acquisition was a bad decision that destroyed shareholder value as they overpaid for a bad business.

By selling the whole construction division, the overall business quality and margin profile will improve.

ROOFING

The core operations of NTBR are roofing. The companies operate via an appropriate contract/order for roofing services.

In order to generate trading profits, the company is required to submit tenders at appropriate prices, manage operational contract delivery, and agree on any variations to the contract with the customer.

The revenues are stable except in periods with a lot of rain and storms like in 2016. Most of the business comes from retrofitting. Margins are much better compared to the construction business above. The margins leave much more room for error. As it is construction-related, we still have the risk of “percentage of completion” accounting.

Cashing out and maintaining the roofing business seems to be the right strategy. The roofing division earned an operating profit of 1.8m that could be used to reallocate into further growth initiatives and acquisitions of better businesses.

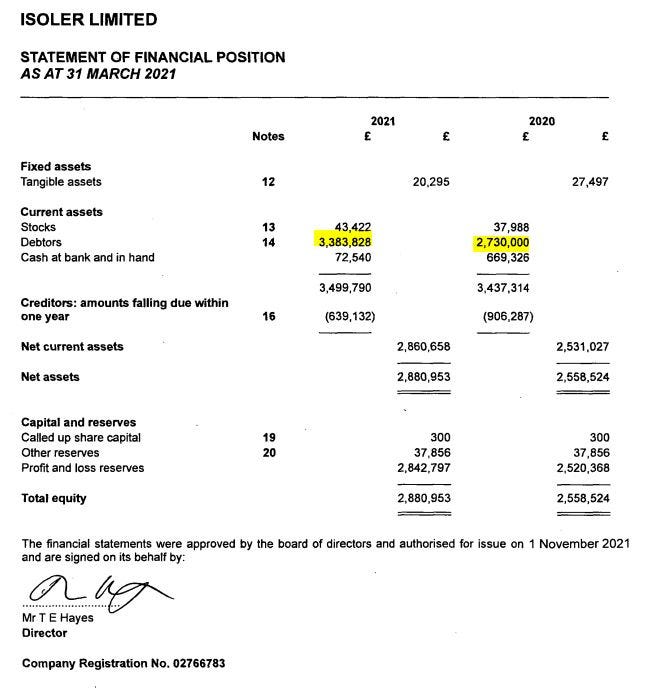

ISOLER

Isoler is a fire protection service company. After the Grenfell Tower tragedy in 2017, where 72 people died, the awareness for fire protection services increased and accelerated the growth rates of the business in 2018 and 2019. Therefore, Isoler benefits from a secular tailwind. The government released new frameworks and invested a billion in 2020 alone in replacing cladding systems. Buildings with a height of 18 meters and above have to comply with new UK regulations.

In the March 2020 budget, the government announced that it will provide £1 billion in 2020 to 2021 to support the remediation of the unsafe non-ACM (aluminum composite material) cladding system on residential buildings 18 meters and over in both the private and social housing sectors.

What you can see is that since 2018/2019 the downtrend has been broken and fire safety investments increased. It would be important to understand how sustainable this trend is.

Isoler alone earned an operating profit of close to a million in 2019 while having huge growth rates. What’s recognizable are the anomalies in 2019 and 2020 where operating margins reached 20,40% and 14,69%.

I believe that the reason is either within “Percentage of Completion” - accounting or the increased demand for fire safety.

Revenues increased by 50% in the same period while receivables grew by just ca. 10%. That would imply that ISOLER booked less revenue in the prior period and more in the following. A 20% margin is therefore not sustainable and I assume that a 10% margin is a much better going forward assumption.

The increased demand would imply that ISOLER was able to negotiate better contract terms and customers started to pay upfront.

What I do not like here is that ISOLER’s revenue decreased by 16,80% 2020/2021 while receivables grew by 24% pointing to a red flag and implying that Isoler booked more revenue than it has earned in the same period.

By adjusting revenues by receivables it would imply that 1.090m have been booked too much and at a 33% gross margin it would imply that ISOLER has recognized 360k EBIT that did not bring any cash in.

Without that the business was barely break-even in that period. I will not put a big weighting on this for now and might update on this information as soon as I understand what’s the reason.

On top of that, I am still working on understanding why the revenue grew by just 8% in 2019/2020 vs 56% and 49% in the prior periods.

Nevertheless, it seems that Isoler is the best performing business unit at NTBR with a very good margin profile and historical high growth rates benefiting from a change in law and governmental subsidies.

If growth rates are sustainable, It could make sense to further invest in the fire safety segment. On top of that, there are more than 900 companies in fire safety that might be worth exploring for acquisitions.

Part III

Part II provided you with a better understanding of which assets are core and non-core. Which are good and which aren’t and what might be a good going forward strategy for those.

Where's part 3? :D